Surplus funds recovery looks simple from the outside: find unclaimed money, connect owners with it, collect a fee. But agents who have worked even a few cases know the reality is far more layered. Part-time agents can earn $36,000–$72,000 annually, yet that income depends on mastering compliance, contracts, outreach, and filing workflows across states with very different rules. Whether you are just starting out or running a small firm, understanding the business models, revenue structures, and tools available to you is what separates agents who close claims consistently from those who stall out after a few wins. This guide breaks all of it down.

Table of Contents

- How recovery agency business models actually work

- Key workflows and methodologies for efficient claims

- Compliance, risk, and legal requirements every agent must navigate

- Paths to scale: From solo agent to high-volume recovery business

- A fresh perspective: What most recovery agents still miss

- Solutions for streamlined surplus funds operations

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Contingency fees dominate | Recovery agents mostly charge a percentage of recovered funds with strict state limits. |

| Efficient workflow is critical | Using the right tech and outreach methods greatly improves claim success and scale. |

| Compliance protects your income | Smart contract clauses, deadline tracking, and legal tech shield agents from costly mistakes. |

| Profit and growth are possible | Solo agents and small firms can generate six figures by automating and expanding strategically. |

How recovery agency business models actually work

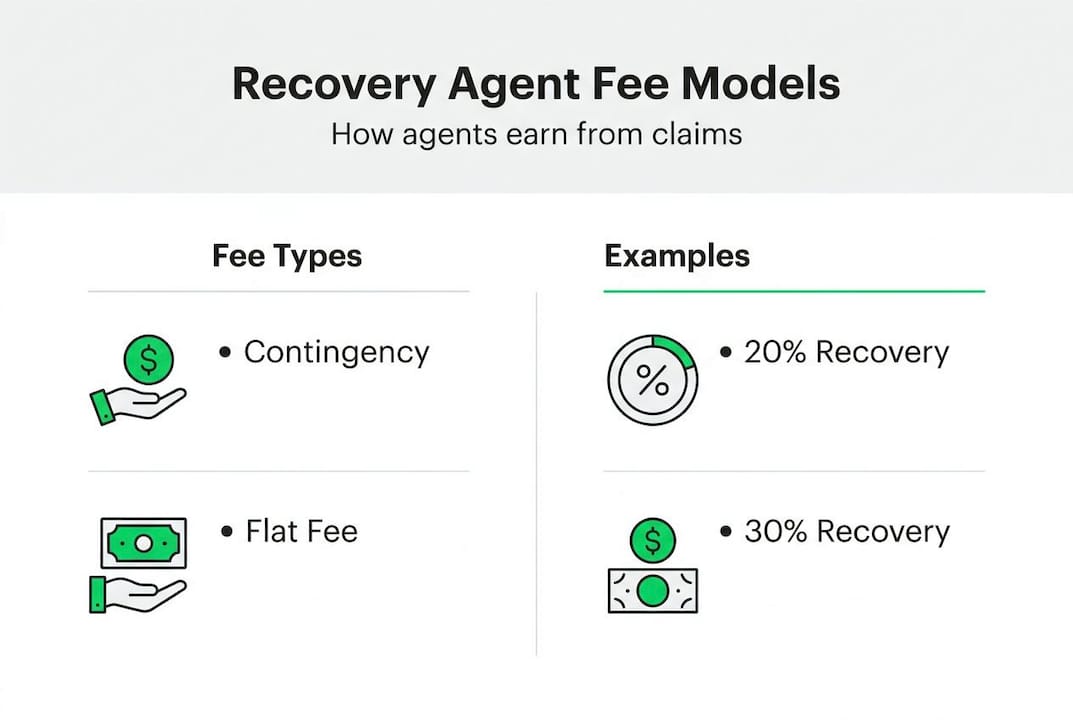

Once you have glimpsed the earning potential and complexity, it is vital to understand what the actual business model entails. At its core, surplus funds recovery is a contingency-based service. You locate surplus proceeds from tax sales, sheriff sales, or foreclosure auctions, identify the rightful owner, and file a claim on their behalf. Your compensation comes only when the claim is paid.

The contingency fee model is the industry standard for good reason: it removes upfront cost barriers for property owners and aligns your incentive with theirs. Most agents charge between 10% and 35% of recovered funds, though state law often sets a ceiling. Florida, for example, caps fees at 12% for certain claim types. Georgia has its own restrictions. Ignoring these caps is not just a legal risk, it is one of the clearest signals that an operation is running outside ethical bounds.

Here is how a typical claim moves from start to finish:

- Source the list: Obtain surplus fund records from county clerks, court systems, or aggregated databases.

- Skip trace: Locate the current address and contact information for the former property owner.

- Outreach: Contact the owner by phone, mail, or SMS to explain the situation and offer your services.

- Agreement: Execute a signed contract that specifies your fee and protects your right to compensation.

- Filing: Submit the claim with required documentation to the appropriate court or government office.

- Payout: Once approved, the funds are disbursed and your fee is collected.

| Claim size | Fee at 20% | Fee at 30% |

|---|---|---|

| $5,000 | $1,000 | $1,500 |

| $15,000 | $3,000 | $4,500 |

| $40,000 | $8,000 | $12,000 |

Full-time agents closing 3–6 claims per month can generate six-figure annual income. Part-time agents working 10–15 hours per week often process 2–4 claims monthly, which is still a meaningful income stream with low overhead.

Pro Tip: Always include a clause in your contract that protects your fee even if the owner redeems the property before the claim is paid. Without it, you could complete all the work and walk away with nothing.

For a broader look at how the recovery workflow overview connects each step, reviewing a structured process guide can help you spot gaps in your own pipeline.

Key workflows and methodologies for efficient claims

Now that you know the basic structure, let's dig deeper into what sets efficient agents and firms apart: powerful workflows. The difference between an agent closing 2 claims a month and one closing 8 is rarely luck. It is process.

A modern, tech-powered workflow looks like this:

- List acquisition: Pull surplus data from county records or a shared lead pool with crowd-sourced intelligence.

- Skip tracing: Use automated tools to find owner contact details quickly and accurately.

- Multi-channel outreach: Contact owners by phone, direct mail, and SMS. Studies show that combining channels significantly increases response rates.

- Contract execution: Send agreements via e-sign platforms to reduce turnaround from days to hours.

- Document preparation: Use AI-powered extraction to auto-fill affidavits and filing packets.

- Claim submission: File with the correct court or agency, tracking deadlines by state.

- Follow-up and payout: Monitor claim status and communicate updates to clients through a self-serve portal.

| Workflow type | Time per claim | Error rate | Conversion rate |

|---|---|---|---|

| Manual | 12–20 hours | High | ~15–25% |

| Tech-powered | 4–7 hours | Low | ~35–50% |

The workflow steps from list sourcing to filing are well documented, but execution is where most agents lose time. Manual skip tracing alone can eat 3–4 hours per lead. Automating that step frees you to focus on outreach and closing.

Hybrid outreach is particularly effective. A phone call establishes trust. A follow-up letter provides something tangible. An SMS reminder nudges action. Together, they produce better results than any single channel alone.

Pro Tip: Hire a virtual assistant to handle initial outreach calls and mail preparation. This lets you focus on contracts and filings, the steps that directly drive revenue. A good VA can handle 20–30 contacts per day, which is volume most solo agents cannot sustain alone.

Using a dedicated CRM for recovery agents keeps every case organized, every deadline visible, and every client communication logged. Without it, cases slip through the cracks.

Compliance, risk, and legal requirements every agent must navigate

Optimizing workflow is great, but there is a hard regulatory boundary every agent must respect: compliance and legal risk. This is the area where agents most often get into trouble, and where the costs of mistakes are highest.

Licensing varies significantly by state. Some states require a private investigator license to perform skip tracing or locate owners. Others require agent registration or business licensing specific to recovery work. Operating without the correct license exposes you to fines and could void your contracts entirely.

DNC compliance is another major risk. The Do-Not-Call registry applies to outreach calls, and violations can result in fines of up to $51,744 per call. Scrubbing your contact lists before every outreach campaign is not optional. It is a baseline requirement.

Here are the compliance areas most agents overlook:

- Redemption clauses: If a property owner redeems their property, your claim may be voided. Your contract must address this scenario explicitly.

- Competing claimants: Heirs, lienholders, and other parties may file competing claims. Know how to handle priority disputes in your target states.

- Filing deadlines: Claim windows vary widely. Some states give claimants 1–2 years; others have windows as short as 90 days. Missing a deadline means losing the claim entirely.

- Escheatment risk: Unclaimed funds eventually revert to the state. If you are working a case close to that threshold, urgency is critical.

"A poorly written contract is one of the most expensive mistakes a recovery agent can make. One missing clause can cost you thousands on a single claim." This is exactly what contract clause oversights in real cases have shown.

The compliance factors around licensing and contracts are not one-time checkboxes. They require ongoing attention as state laws change. Building a compliance review into your quarterly operations is a smart practice.

For agents looking to stay ahead of regulatory shifts, legal tech solutions for agents that include a 50-state compliance engine can reduce the burden of manual tracking significantly.

Paths to scale: From solo agent to high-volume recovery business

With a handle on workflow and compliance, the next frontier is scaling up. Let's examine how to turn solo efforts into a sustainable business.

Most solo agents hit a ceiling around 4–6 active cases at a time. Beyond that, research, outreach, and filing demands exceed what one person can manage without dropping quality. Scaling requires deliberate decisions about people, markets, and systems.

Hiring virtual assistants is the first and most accessible step. VAs can handle list research, skip tracing, initial outreach, and document preparation. This frees you to focus on contracts and filings, the highest-value activities. A well-trained VA costs $8–$20 per hour and can support 3–5x your current case volume.

| Operating cost | Monthly estimate |

|---|---|

| VA (part-time) | $800–$1,600 |

| CRM and tools | $100–$400 |

| Skip tracing data | $50–$200 |

| Postage and mail | $100–$300 |

One average claim at $15,000 with a 25% fee generates $3,750, which covers most of these costs for an entire month. The margin on surplus recovery, when managed well, is strong.

Market selection matters enormously. Florida, Georgia, and Texas are consistently active markets with high claim volumes and accessible public records. Workflow automation paired with smart market selection is how high-volume agencies build their pipelines.

Here are the top steps for building a scalable agency:

- Standardize your intake and outreach process with templates and automation.

- Hire and train a VA before you feel overwhelmed, not after.

- Focus on 2–3 high-volume states before expanding geographically.

- Build referral relationships with attorneys who handle probate and estate work.

- Track your conversion rate by state and lead source to identify what is working.

Some agents explore nonprofit or attorney-led models. Nonprofits can build public trust and access certain claim types more easily, but they come with governance requirements and restrictions on fee structures. Attorney-led models benefit from established trust signals and can handle complex competing-claim scenarios, but require legal partnerships that take time to build.

The benchmarks for operating costs and conversion rates show that agents using integrated tools consistently outperform those relying on spreadsheets and manual processes. The gap widens as volume increases. Reviewing growth strategies for agents can help you identify the right next step for your specific situation.

A fresh perspective: What most recovery agents still miss

Across all these structures, what truly separates successful agencies is not obvious, and it is where most newcomers stumble. The common assumption is that success comes from finding more leads. In practice, it comes from protecting the leads you already have.

Agents routinely underestimate two things: their legal exposure and the compounding cost of manual workflows. A contract without a redemption clause, a missed DNC scrub, or a filing deadline overlooked by a day can erase weeks of work. These are not edge cases. They happen regularly.

The agents building durable businesses are doubling down on smart workflow automations and airtight contract language simultaneously. They treat compliance as a competitive advantage, not a burden. Clients refer others when they feel protected and informed.

Hybrid models, where a for-profit agency collaborates with a nonprofit or attorney partner, are also underused. They open access to claim types and client segments that a solo for-profit agent cannot reach alone. This is a real growth lever that most agents have not explored.

Owning both the compliance side and the client experience side of your operation is what makes an agency defensible at scale. Volume without systems creates chaos. Systems without client trust create churn.

Solutions for streamlined surplus funds operations

Turning insight into action starts with the right partner, especially when it comes to scaling smarter and staying compliant. TENNO Recovery is built specifically for agents like you, combining CRM, DNC compliance, skip tracing, and workflow automation into one platform.

With the TENNO RECOVERY platform, you can manage your entire pipeline from lead to payout, generate county-specific filing packets, and keep clients informed through a self-serve portal. The 50-state compliance engine takes the guesswork out of licensing and deadline tracking. Want to see exactly how it fits your operation? See how our process works or take the next step and apply as an agent today.

Frequently asked questions

What is the typical fee structure for surplus funds recovery agents?

Most agents charge a contingency fee of 10–35% of recovered funds, but state laws often set maximums. Florida, for example, allows up to 12% for certain claim types.

Do I need a license to operate as a recovery agent?

Some states require a private investigator license or agent registration, so check local licensing requirements before starting operations in any new state.

How do recovery agents find surplus funds leads?

Agents typically source surplus lists from county records or court systems, then use skip tracing tools to locate and contact property owners.

What are the most common risks for recovery agents?

The biggest risks include property owner redemption voiding your claim, competing claimants, and state-specific filing deadlines that can vary widely and are easy to miss.

Can surplus funds recovery be done part-time?

Yes. Part-time agents processing 2–4 claims monthly can earn $36,000–$72,000 annually with relatively low operating costs and flexible hours.