Document errors and omissions are the leading reasons surplus funds claims get denied or delayed, costing agents weeks of rework and lost revenue. Whether you're filing against a tax sale or a sheriff sale, the difference between a fast approval and a frustrating rejection almost always comes down to paperwork. This guide walks you through exactly which documents to prepare, how to secure proper authorization, how to navigate the filing process step by step, and how to handle the edge cases that trip up even experienced agents. Follow this blueprint and you'll spend less time correcting mistakes and more time closing claims.

Table of Contents

- Core documents and agent preparation

- Assignment agreements and fee compliance

- Filing the claim: Steps, process, and timelines

- Troubleshooting: Edge cases and delays

- Why most agents overlook documentation and how pros create efficiency

- Simplify your surplus claim workflow with TENNO Recovery

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start with the right docs | Collect all identity and ownership proof plus any required probate documents before starting your claim. |

| Use compliant agreements | Written authorization and correct fee structures keep claims legal and approved. |

| Follow local rules | Court and trustee processes differ by state and county, affecting timelines and requirements. |

| Troubleshoot smartly | Know how to address heirs, liens, and delays to keep your pipeline moving. |

| Efficiency leads to success | Systematizing your documentation and workflow is the real key to increased revenue and fewer denials. |

Core documents and agent preparation

Getting your documentation right before you file is the single most important thing you can do to protect your approval rate. Agents who skip this step often discover missing items after submission, which restarts the clock and frustrates claimants. A few minutes of upfront preparation saves weeks of back-and-forth.

Core documentation for surplus funds claims includes a government-issued photo ID, proof of ownership or recorded interest such as a deed or tax records, and for heirs: a death certificate, probate documents, an affidavit of heirship, or letters of administration. Each of these serves a specific legal function, so a missing item is not a minor inconvenience. It is a denial waiting to happen.

Here is a quick breakdown of document requirements by claimant type:

| Claimant type | Required documents |

|---|---|

| Original property owner | Photo ID, deed or tax record, sale confirmation |

| Heir (with probate) | Photo ID, death certificate, letters of administration |

| Heir (without probate) | Photo ID, death certificate, affidavit of heirship |

| Estate representative | Photo ID, letters testamentary, probate court order |

Beyond the basics, efficient agents build preparation checklists tailored to each state and county. County-specific checklists help you avoid the guesswork of figuring out what a particular clerk's office requires. You can also reference state-specific documentation requirements to confirm any variations before you start gathering materials.

Key preparation habits that reduce errors:

- Use a digital folder system organized by case ID and claimant name

- Collect property sale records and tax history at the same time you pull ownership docs

- Run skip tracing early if a claimant is hard to reach, so you are not waiting on ID verification at the last minute

- Confirm notarization requirements for affidavits before printing final versions

- Cross-check every name spelling against the official property record

Pro Tip: Create a master checklist template for each state you work in and update it whenever a county changes its requirements. This single habit can cut your document prep time by 30% or more per case.

Assignment agreements and fee compliance

Once your documents are in order, the next critical step is securing the right agreements and staying on the right side of the law. Filing a claim without a written authorization from your claimant is not just risky. It can void your fee entirely and expose you to legal liability.

Written assignment agreements are mandatory before acting for a claimant. These agreements authorize you to recover funds on a contingency basis, with typical contingency fees ranging from 10% to 35% depending on the state and the complexity of the case. Georgia, for example, caps fees at 15% for claims under $25,000. Florida and California have their own rules that you must verify before signing any agreement.

Here is a comparison of fee structures across key states:

| State | Fee cap | Notes |

|---|---|---|

| Georgia | 15% (claims under $25k) | Statutory cap, strict enforcement |

| Florida | Varies by contract | No hard cap, but court scrutiny applies |

| California | Negotiated | Attorney involvement often required |

| Texas | Negotiated | Agent must disclose fee in writing |

Steps to stay compliant with assignment agreements:

- Draft a written contingency agreement before any contact with courts or trustees

- Include the exact fee percentage, the specific property, and the claimant's full legal name

- Have the agreement reviewed by a licensed attorney in states that require attorney oversight

- Provide the claimant with a plain-language explanation of what they will net after your fee

- Retain a signed copy in your case file and a backup in your digital repository

Understanding how agent agreements work is critical not just for compliance but for building trust with claimants. When you explain fees clearly and in writing, claimants are far more likely to cooperate throughout the process.

Pro Tip: In states with attorney oversight requirements, build a relationship with a local attorney who can co-sign or review agreements in bulk. This speeds up your workflow without adding significant cost per case.

Filing the claim: Steps, process, and timelines

You're authorized. Now let's break down exactly how to file and follow your claim through to approval.

The filing process varies by state and sale type, but the core steps are consistent. Submitting a verified motion or petition to the clerk of court or trustee is the central action, and it must include all supporting documents. In judicial foreclosure states, a court hearing may be required. In non-judicial states, the trustee often handles distribution without a hearing.

Step-by-step filing process:

- Assemble your complete documentation packet, including ID, ownership proof, and authorization agreement

- Draft a verified petition or motion that identifies the claimant, the property, and the surplus amount

- Submit the packet to the appropriate court clerk or trustee, paying any required filing fees

- Serve all interested parties, including junior lienholders, as required by state law

- Attend any scheduled court hearing and present your documentation if challenged

- Follow up with the clerk or trustee at regular intervals until disbursement is confirmed

Timeline expectations vary significantly by state and process type:

| State/process | Typical timeline | Notes |

|---|---|---|

| Florida (court registry) | 30 to 90 days post-approval | Judicial process, hearings common |

| California (trustee) | 30 days | Non-judicial, faster turnaround |

| Georgia (tax sale) | 60 to 120 days | Redemption period affects timing |

| General average | 30 to 120 days | Claim process timelines vary widely |

Key fact: Surplus funds are distributed in a specific priority order. Sale costs and court fees come first, then senior liens, then junior liens, and finally the former property owner or their heirs. Knowing this order helps you set realistic expectations with claimants.

Understanding the filing process in your target states is not optional. Agents who treat every state the same make costly errors that delay payouts by months.

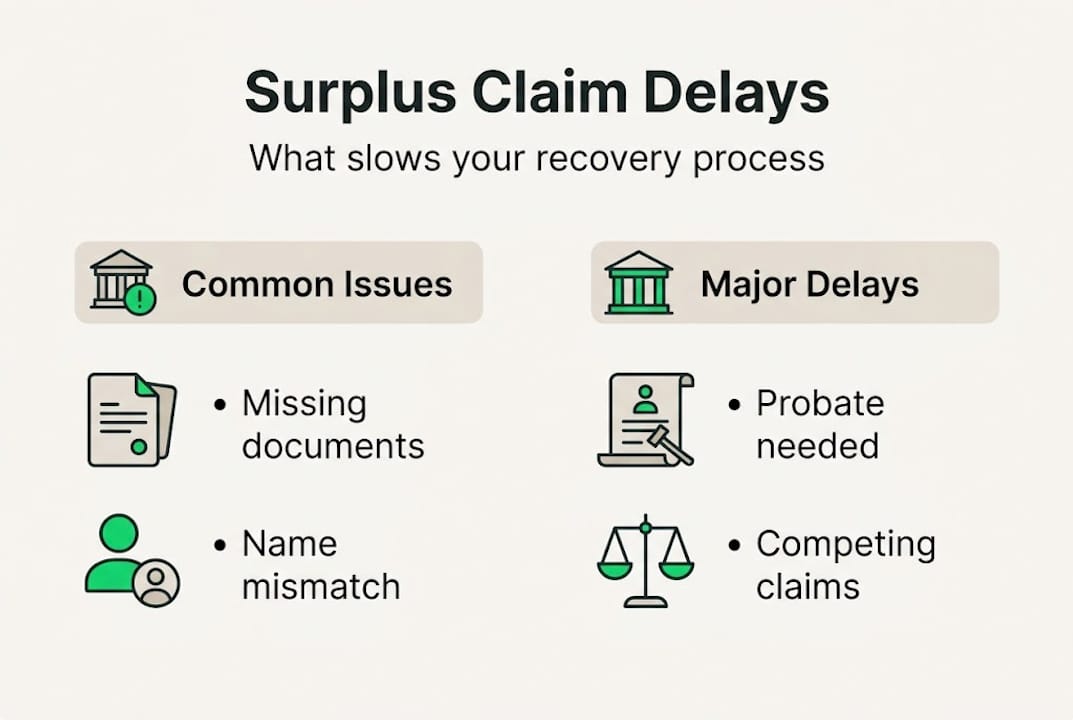

Troubleshooting: Edge cases and delays

No two claims are alike. Here's how to troubleshoot common edge cases and keep your pipeline moving.

The most frequent complications agents face involve deceased owners, competing claimants, and funds that have already escheated to the state. Heir claims require probate or estate documents, competing claims from liens or multiple heirs trigger formal hearings, and deceased owners require successors to establish legal standing before any distribution can occur.

Common edge cases and how to handle them:

- Deceased owner with no probate: File for a small estate affidavit if the state allows it, or guide the family through a simplified probate process before filing the surplus claim

- Multiple heirs with no agreement: All heirs must typically sign off or be served notice; a court may appoint a representative if heirs cannot agree

- Junior lienholder competing for funds: Verify lien priority using the distribution order after a sheriff sale and include lien payoff documentation in your packet

- Missing claimant: Use skip tracing tools early and document your search efforts in case the court asks for proof of due diligence

- Funds already escheated: Contact the state's unclaimed property division directly; most states allow recovery through a separate claim process even after escheatment

"Escheated funds follow the unclaimed property process, but they are not permanently lost. Authorized parties can still recover them, though the process adds significant time and paperwork."

Delay scenarios are frustrating but manageable. Name discrepancies between the deed and the claimant's ID, unresolved federal tax liens, and incomplete service of process are the most common causes of extended timelines. Address these issues proactively by managing legal complications before they become rejections.

Realistic delay ranges: minor documentation issues add 2 to 4 weeks; probate complications add 3 to 6 months; competing claims with hearings can add 6 to 12 months. Build these ranges into your client communications from day one.

Why most agents overlook documentation and how pros create efficiency

Here is an uncomfortable truth: most agents who struggle with claim denials are not making legal errors. They are making organizational ones. The rush to submit a claim before fully assembling the packet is the most common and most avoidable mistake in this business.

Highly productive agents earning $75,000 to $200,000 per year do not get there by working harder on individual claims. They build systems. Templates, digital repositories, and automated follow-up sequences are what separate a 10-claim month from a 40-claim month. The goal is not just to finish one claim. It is to make the next 20 claims faster because the infrastructure already exists.

Many agents treat documentation as a one-time task per case. Pros treat it as a repeatable process. Establishing repeatable documentation systems means every new case slots into a structure that already works, rather than starting from scratch each time.

The agents who consistently hit the top of the earnings range are not luckier or better connected. They have fewer surprises because they have seen every edge case before and already have a response ready. That readiness comes from documentation discipline, not talent.

Simplify your surplus claim workflow with TENNO Recovery

If you're ready to apply these best practices with fewer headaches, here's how to take the next step.

TENNO Recovery gives independent agents the tools to execute every step in this guide faster and with greater accuracy. From county-specific filing packet generation to a 50-state compliance engine that flags fee cap violations before you sign an agreement, the platform is built around the exact pain points this guide addresses.

Agents who become a TENNO Recovery agent get access to AI-powered document extraction, auto-filled affidavits, and a shared lead pool with crowd-sourced intel across all 50 states. If you want to understand how it works before committing, the platform walkthrough covers everything from onboarding to your first filed claim. Stop rebuilding your process from scratch on every case and start working from a system that scales.

Frequently asked questions

What documents are essential for every surplus funds claim?

You always need a government-issued photo ID and proof of ownership; claims involving heirs also require probate documents or a signed affidavit of heirship to establish legal standing.

How long does the surplus funds claim process usually take?

Most claims are processed in 30 to 120 days, but state and county rules, along with probate or lien complications, can push timelines well beyond that range.

What can delay a surplus claim payout?

Common causes include missing documents, competing heirs or liens, unresolved probate, name discrepancies between records, and state-mandated waiting periods that cannot be waived.

How do state fee limits impact my agency's surplus recovery agreements?

You must set your contingency fee within your state's cap before signing any agreement; Georgia, for example, limits fees to 15% for claims under $25,000, and violating this cap can void your contract entirely.

What happens if funds go unclaimed?

Unclaimed surplus funds escheat to the state through the unclaimed property process, but heirs or authorized parties can typically recover them later by filing a separate claim with the state's unclaimed property division.